Economic Report

The income contraction experienced in 2022 and 2023 was driven by the supply growth of available listings outpacing travel demand. During 2021 and 2022, supply surged as investors sought to capitalize on low interest rates, stimulus, and pent-up travel demand in the U.S. This led to one of the most significant contractions in revenue per available rental (RevPAR) on record.

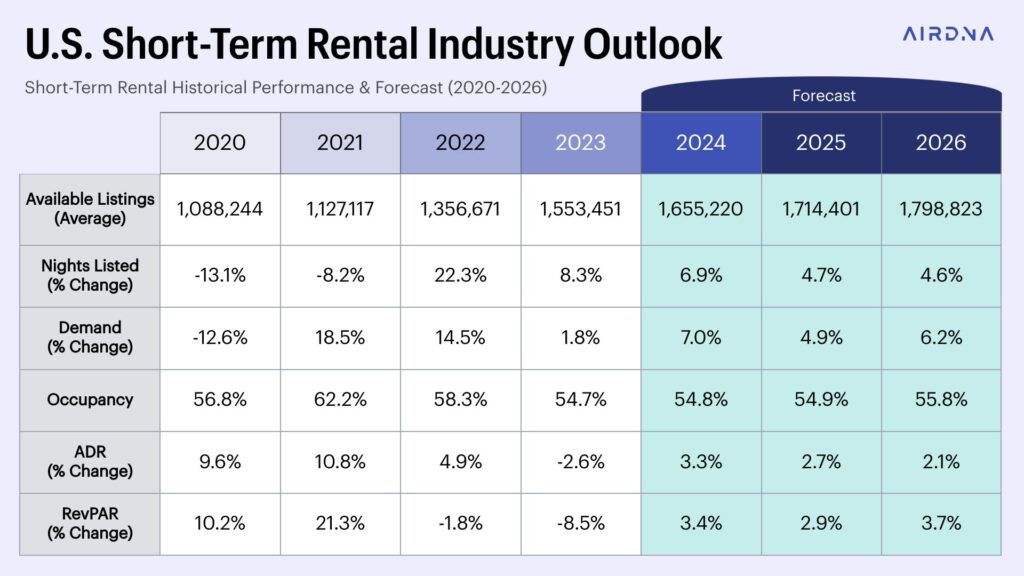

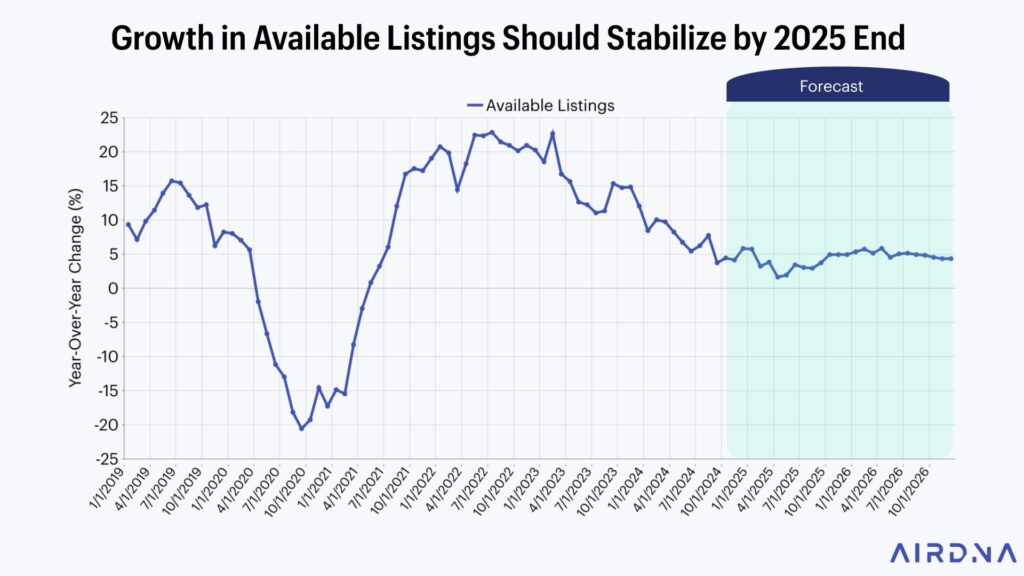

Since then, Unwind has closely tracked supply growth and demand trends to assess signs of recovery. As shown in the table below, nights listed grew by 6.9% in 2024 and are projected to increase by 4.7% in 2025 and 4.6% in 2026. More importantly, the row below highlights the year-over-year demand increase. In 2022 and 2023, supply growth (nights listed) significantly outpaced demand growth. However, in 2024, demand growth exceeded supply growth, and this trend is expected to widen further in 2025 and 2026 based on current economic indicators.

Though the shift will be gradual, this is encouraging news for STR owners. As available listing growth slows and demand outpaces supply growth, occupancy rates and RevPAR should rise over the next two years just as they did in 2024.

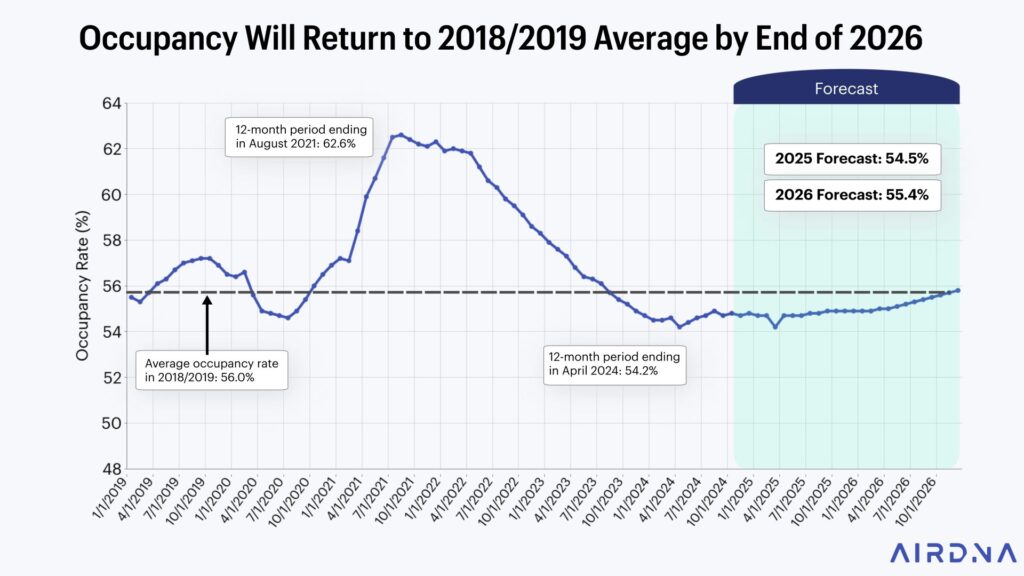

Additionally, as seen in the table below, supply growth has decelerated more rapidly in small and mid-size cities and Mountain/Lake markets compared to Large Urban and Coastal markets. While the benefits of demand growth exceeding supply growth will vary by location, the overall trend is positive for investors, and as you will see in the graph below, we expect occupancy levels will recover to their pre-covid levels by 2026.

Similarly, high interest rates have had only a marginal impact on home prices. While the revenue contraction in 2023 and 2024 posed challenges for many, it did not trigger the price correction that some economists had anticipated. Despite rising borrowing costs, home prices remained resilient, and by 2024, we observed a renewed upward trajectory in valuations.

As illustrated in the graph below, the home price index exhibited only a minor response to rising rates, and home prices are projected to double between Q1 2018 and Q4 2026. This is favorable for existing homeowners, who stand to benefit from sustained appreciation when selling their properties. However, for investors seeking to acquire assets in 2025 and 2026, elevated home prices will likely compress profit margins and necessitate a more strategic approach to capital allocation. As with supply-demand dynamics, the magnitude of these effects will vary across regional markets.

Looking ahead, several macroeconomic factors signal further price appreciation in most markets. The anticipated growth in RevPAR, driven by a more favorable supply-demand equilibrium, coupled with resilient asset prices, moderating inflation, and the Federal Reserve’s December 2024 projection of two 25-basis-point rate reductions in 2025, collectively create conditions for continued price expansion. These factors should support stronger investor confidence, enhance property valuations, and present opportunities for strategic exits at attractive price points over the next two years. However, investors should remain mindful of regional disparities and evolving market conditions when assessing long-term return potential.